Selecting Your Business Structure

This page is dedicated to helping you select the best structure for your business. Through this exercise, you'll actually make two separate, but related, decisions: legal structure and tax treatment.

- Jump To:

- Overview

- Business Structure Comparison Chart

- Tax Treatment Comparison Chart

- Legal Structure vs Tax Treatment Chart

- 5 Considerations to Help a Small Businesses Select a Business Structure

Overview

Choosing a business structure involves two interrelated decisions: one decision on legal structure and one decision on tax treatment. While vocabulary like "an LLC taxed as an S-Corp" can be daunting at first, you'll soon master the vocabulary of the most common legal structures (sole proprietorship, partnership, limited liability company, and corporation) and tax treatments (disregarded entity, S-Corp, and C-Corp). Use our comparison charts to navigate these options. You'll discover what legal structure is the best fit for your endeavor and which tax treatment is most advantageous.

Choosing the correct business structure enables long-term success. Depending on your needs, you might choose a structure optimal for:

- Limiting legal liability

- Gaining fellow owner-operators

- Attracting passive investors

- Saving money on taxes

- Saving on start-up expenses

- Avoiding burdensome administrative duties

- Executing your exit plan such as a transfer or sale

This page provides general education on the most common options. Please seek the guidance of a licensed attorney or accountant for personalized advice.

Business Structure Comparison Chart

The chart below compares the most popular business structures.

| Sole Proprietorship | Partnership (GP or LP) |

Limited Liability Company (LLC) |

Corporation (C-Corp or S-Corp) |

|

|---|---|---|---|---|

|

Summary |

This structure is owned and operated by a single individual. It is simple, low cost, and fast to set up. No separate legal entity is created. The sole proprietor is exposed to unlimited liability; lawsuits against the business likely put personal assets at risk and vice versa. |

A business owned and operated between two or more people. In a general partnership (GP), all parties are typically owner-operators. Rights and duties are typically proportional to ownership. A limited partnership (LP) consists of one general partner with unlimited liability who manages the business and one or more limited partners who behave as silent investors. |

LLCs are popular for good reason. LLCs combine the liability protections of corporations with the pass-through taxation available to sole proprietors and partnerships. |

Businesses that will immediately earn substantial revenue or involve complex ownership arrangements typically consider a corporation or an LLC taxed as a corporation. C-Corp and S-Corp are not legal structures. They refer to two tax elections that can be made for either an LLC or a corporation. Colloquially, an "S-Corp" refers to a corporation taxed as an S-Corp, and similar for "C-Corp". |

|

Number of Owners |

1 | 2 or more |

Most states allow single-member LLCs, but some require 2+ members. LLCs that elect S-Corp taxation may have no more than 100 shareholders and face other IRS restrictions. |

Corporations may have a single shareholders. C-Corps can have unlimited shareholders. S-Corps may have no more than 100 shareholders and face other IRS restrictions. |

|

Control |

The owner has total control of business operations and profits. | Partners define the management and profit-sharing of the business in a document called the Partnership Agreement. Owners in a GP have total control of business operations and profits. Only general partners in an LP may exercise control. | An LLC is owned by members who receive profits per their ownership percentage or as defined in the Operating Agreement. The members can manage the LLC themselves, known as "member-managed", or can declare the LLC “manager-managed” and appoint managers. | Most often a corporation issues stock to shareholders who invest in the corporation in anticipation of profit. Shareholders elect a board of directors to oversee the corporation. In smaller corporations, one person may hold multiple positions. |

|

Limited Liability |

No. The owner's personal assets are at risk. |

GP: No. Each partner is liable for the decisions of the other(s). LP: Limited partners may only act as investors. General partners may participate in management decisions but lack liability protection. |

Yes. Members are protected from the liabilities of the business. | Yes. Shareholders, officers, and directors are protected from the liabilities of the business. |

|

Taxation |

Income or loss is passed through to the owner. | The business is taxed as a partnership. Income or loss is passed through to the owners. | Most small businesses start with pass-through taxation (the same as a sole proprietorship or partnership). The LLC may make a special election to be taxed as an S-Corp or C-Corp, which helps save on taxes as the business grows. | By default, the corporation is taxed as a C-Corp. This results in double taxation of corporate profit and distributions to shareholders. Many small businesses choose to elect S-Corp taxation so the corporation is taxed as a pass-through entity (like a partnership). |

| Transfer of Ownership | No. Cannot be transferred or sold. Business dissolves upon owner's death. | Based on Partnership Agreement. | Yes | Yes |

| How to Start |

|

|

|

|

Other Legal Structures

The chart above showcases only the most popular business strcutures. There are many other more specialized business structures, often intended for a specific purpose.

- Nonprofit Corporation & other nonprofit structures

- If your organization has an altruistic mission, setting up a legal and tax structure is a key step in formalizing support for your cause. It is most common for a nonprofit to form a nonprofit corporation, though some states also permit nonprofit LLCs, nonprofit trusts, and unincorporated nonprofit associations. After incorporating, you can apply for 501(c) and other tax exemptions.

- Limited Liability Partnership (LLP) and Limited Liability Limited Partnership (LLLP)

- Generally speaking, partners in an LLP are shielded from debts, obligations, and liabilities resulting from another partner's negligence, malpractice, or misconduct. This makes them different than GPs and LPs; they afford some or all partners limited liability (depending on the jurisdiction). Generally, whereas a GP or LP requires a partner with unlimited liability, the LLP and LLLP do not. These structures are popular with (and in some states expressly limited to) lawyers, accountants, and other licensed professionals.

- Professional Corporation (PC), Professional LLC (PLLC), Professional LLP

- Attorneys, doctors, accountants, and other licensed professionals are restricted in which legal entities they are permitted to form. Restrictions vary by state and options often include a professional corporation, professional LLC, or professional LLP.

- Close Corporation

- Close corporations and similar entities are “closely held”. They owned by a small number of private parties such as family members.

- B-Corporation

- A Benefit Corporation (B-Corp) is basically a for-profit corporation dedicated to a nonprofit cause. This relatively new type of corporation seeks to attain public benefit, environmental benefit, employee benefit, other social benefit; holds to standard in transparency of operations; and often obtains third-party certification.

Tax Treatment Comparison Chart

| Partnership | S-Corp Taxation | C-Corp Taxation | |

|---|---|---|---|

|

Summary |

The business does not pay corporate taxes; instead all profits, losses, deductions, and credits are reported on the owners’ tax returns and business tax is paid at the personal income tax rate. | Like a pass-through entity, all profits, losses, deductions, and credits are reported on the owners’ tax returns and business tax is paid at the personal income tax rate. Owner-employees realize savings on self-employment taxes. S corporations are responsible for tax on certain built-in gains and passive income. | C-Corporations suffer from double taxation: the corporation pays taxes on profits then shareholders pay taxes on their distributions. C-Corp taxation is appropriate when the benefits of deducting employee contributions and income splitting outweigh the costs of double taxation. Small businesses that will re-invest most of their profits in the business can benefit from the low tax rates on retained earnings. |

|

Rule of Thumb |

Best when <$75,000 profits per owner | Best when $75,000-$250,000 profits per owner | Best when $250,000+ profits per owner |

|

Tax Forms and Rate |

Businesses with more than one owner file an informational return of the allocation

amongst owners (Form 1065). Each owner reports his share of company profits, losses, deductions, and credits on his personal income tax return (often Schedule 1040 Schedule C). You will pay taxes for your portion of business earnings at your personal income tax rate. Owner-employees are also responsible for self-employment taxes (15%). |

S corporations are responsible for tax on certain built-in gains and passive income

and must file Form 1120S. Each owner reports his share of company profits, losses, deductions, and credits on his personal income tax return (often Schedule 1040 Schedule C). You will pay taxes for your portion of business earnings at your personal income tax rate. Owner-employees only pay self-employment taxes (15%) on the “reasonable salary” they pay themselves. |

C corporations pay taxes at corporate income

tax rates. This is reported on Form 1120. Each owner reports wages and distributions on his personal income tax return (often Schedule 1040). You will pay taxes only for wages and capital gains at your personal income tax rate. The distributions suffer from corporate double taxation since both you and the corporation are paying taxes on these earnings. Wages are deducted from corporate revenue prior to paying corporate income taxes (they do not suffer from double taxation). The employer and employee each pay their share of employment taxes on wages. |

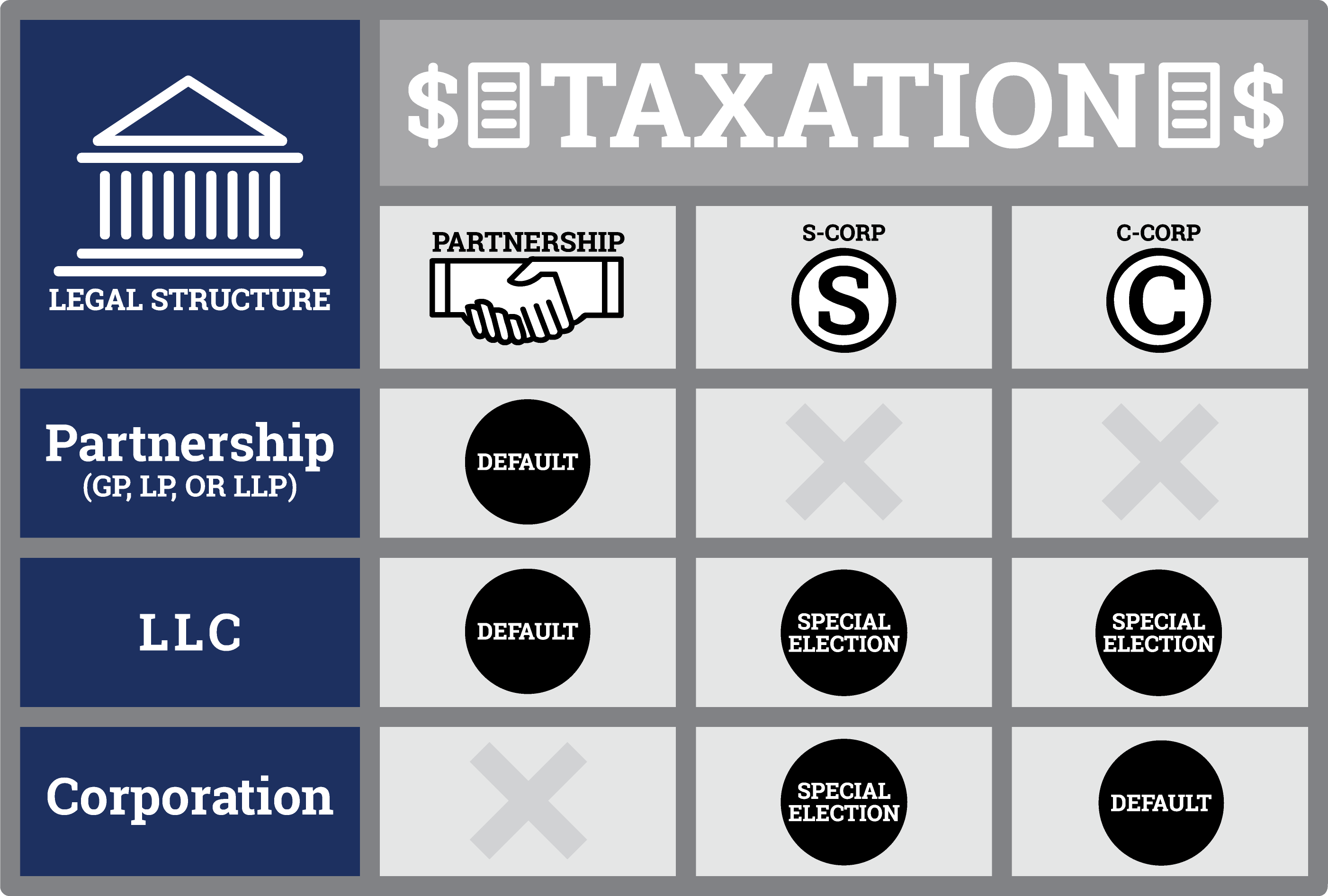

Legal Structure vs Tax Treatment Chart

The following chart shows the most common legal structures and the taxation options available to them.

For example, if you decide you want to be taxed as an S-Corp, you can structure your business as either an LLC or a corporation. It helps to consider your legal structure and desired taxation independently, then refer to this chart to see if your desired combination is available.

5 Considerations to Help a Small Businesses Select a Business Structure

If you're starting a small business and feeling overwhelmed navigating business structures and tax treatments for the first time, you're not alone. This section is written for you. We'll walk though five considerations to help simplify your options.

By "small business", we mean companies with just one or only a few owners. This includes mom-and-pop shops, retail stores, consumer services, and business-to-business services. 90% of small businesses only need to consider two options:

- a sole proprietorship (one owner) or a general partnership (many owners), or

- a limited liability company

These structures are inexpensive to start, easy to run, and permit you to save money on taxes with pass-through taxation.

Here's why the other structures you may have heard about don't make much sense to a new small business:

- LPs, LLPs, and other partnerships are generally used by attorneys, accountants, real estate agents, and other professionals.

- A corporation is typically used for more complex ownership and investment structures. The many formalities of running a corporation make sense when a lot of owners and investors are working together. (What about the benefits of S-Corp tax treatment, you ask? An LLC can be taxed as an S-Corp!)

Consideration #1: Your Business Name

Does your business name include your legal last name? If not, your state likely requires you to register your business name.

Let's use the example of John Doe, who is ready to take his passion for flamingo lawn ornaments and turn it into a business. He would not need to register the name "John Doe's Lawn Ornaments" because it includes his legal name. But he would need to register "Flamingoes Galore Lawn Ornaments" since it doesn't.

To fulfill the requirement to register a business name, you can register either a fictitious name (to start a sole proprietorship or general partnership) or file the formation document for an LLC or other business entity.

Consideration #2: The Importance of Liability Protection

Registering a business entity (such as an LLC) provides the added benefit of limited

liability. Limited liability is what protects your personal assets if the business gets into

debt or is sued. Your home, car, retirement account, and children's college funds stay

yours.

Limited liability should be the chief concern for most owners. Often it is not until owners

discuss their risks that they realize their exposure. Any business with a physical location,

employees, or that sells a product or service that might malfunction (e.g. food poisoning)

has liability risk.

A common misconception is that you don't need limited liability if you purchase liability

insurance. The difference is this: liability

insurance protects the assets of the business while a limited liability entity protects

the assets of the owners. Furthermore, liability insurance can exclude coverage and

set policy limits.

Consideration #3: Comparing Costs and Effort

An LLC is probably not as expensive or time-consuming as you think, compared to running a sole proprietorship or partnership. Many of your basic business practices and fees will be the same.

Forming an running an LLC may be easier than you think:

- Depending on your state, the fee to form an LLC may be less, the same, or slightly more than the fee to register a doing business as (DBA) name. For example, in Pennsylvania a fictitious name costs $270 (due to publishing fees) and an LLC costs $125.

- Regardless of which business structure you choose, you should be running your business as a business. This means keeping separate finances for your business, signing contracts under the business instead of your personal name, and other day-to-day basic business behaviors.

- Many accountants do not charge extra to file your taxes as an LLC. They need to prepare many of the same forms and schedules. By default, an LLC receives pass-through taxation so it will be identical to the taxation you would receive as a sole proprietorship or general partnership.

The extra effort of an LLC:

- Running an LLC means that you should hold an annual meeting. If it's just you, have a meeting with yourself. Take yourself and your business partners out to lunch (on the business), discuss your performance in the past year and plans for the next year, and write meeting minutes for your LLC records.

- Some states charge an annual fee to run an LLC and some do not. This would take the form of an annual report filing, an annual state business license fee, or an annual franchise tax.

Consideration #4: Form your business in the state where you live and work

There is a lot of hype about registering your business in another state such as Delaware. The catch is that if you register your business in another state, you also have to register in your home state. So you would have to pay the expense of setting up and maintaining a business entity with two registrations.

This concept is called foreign qualifying. When you form your business, you will be authorized to do business in the state where your business is registered. When you're ready to start regularly transacting business in another state (or meet other criteria requiring registration), you will need to "foreign quality" in that state to register your business in those borders.

Consideration #5: Most small businesses save money with pass-through taxation

Pass-through taxation means that your business profits, losses, credits, and deductions "pass through" to your personal income tax returns. At the end of the year, you simply add your business income to your personal income then pay all taxes at your personal income tax rate. A sole proprietorship, general partnership, and LLC all receive pass-through taxation by default. In general, an LLC can save on taxes when profits exceed ~$75,000 per year per owner by electing S-Corp taxation.

Next

- Learn more about starting your own business

- Learn more about Incorporation (C-Corp or S-Corp)

- Learn more about Limited Liability Company formation

- Learn more about Series Limited Liability Company formation

- Learn more about Sole Proprietorship formation

- Learn more about General Partnership formation

- Learn more about Limited Partnership formation

- Learn more about Limited Liability Partnership formation

- Learn more about Limited Liability Limited Partnership formation